What if Steve Aoki traded DigiDaigaku call options?

We briefly touched on the perspective of an NFT trader in a previous blog post where we argued call options are value-accretive for the NFT ecosystem. Today we want to expand on that by presenting a simplified case study based on the currently mooning NFT project DigiDaigaku (floor price = 12.46 ETH at press).

Premise

In this blog post we take a snapshot of one DigiDaigaku Genesis trader’s activity - that of the venerable Steve Aoki - and ask the question: What if Steve purchased call options on DigiDaigaku instead of buying them?

Inputs, assumptions, and methodology

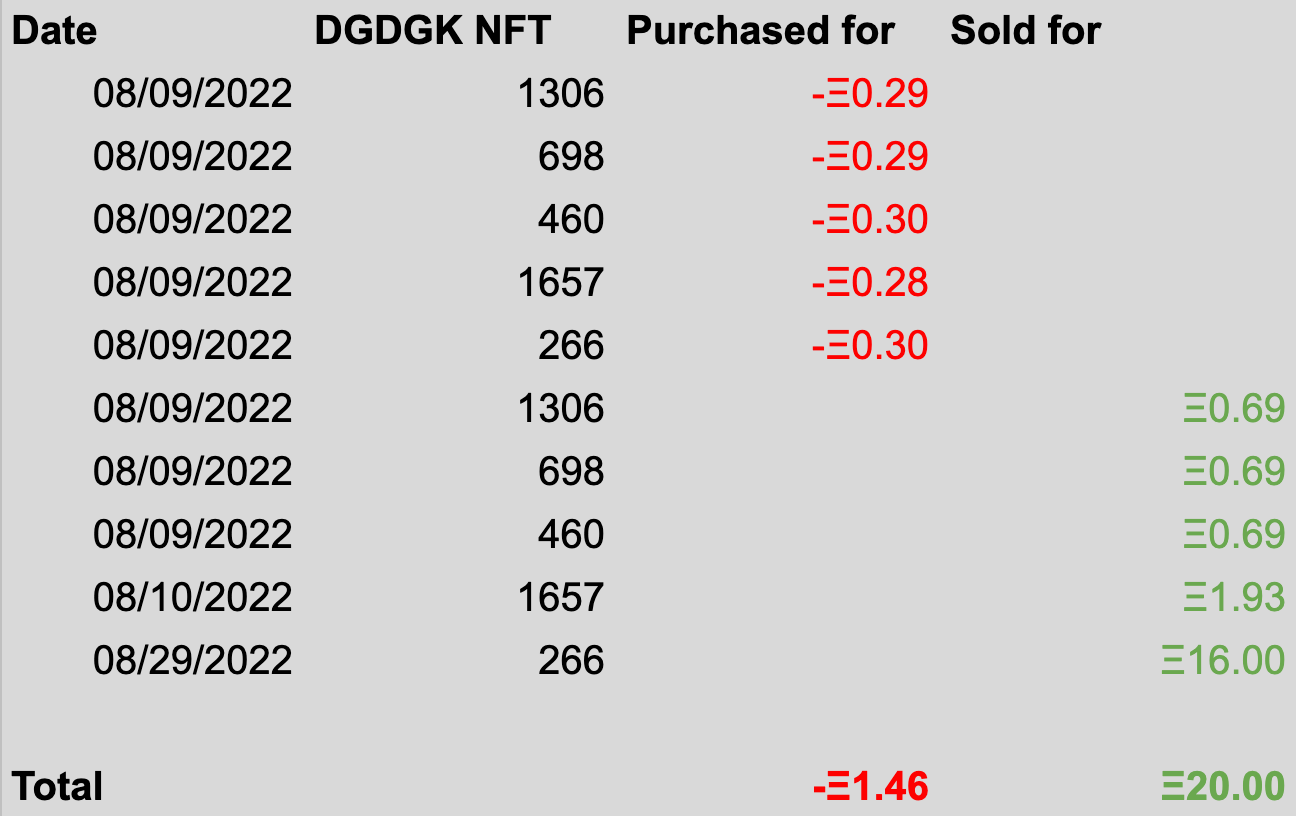

Above is a snapshot of Steve’s trading activity on DigiDaigaku (“DGDGK”) as of Sep 1st, 2022 from OpenSea. #1404, 1107, and 166 have not yet been sold, so we will exclude them from our analysis:

The Black-Scholes model for option pricing is the most widely accepted and used formula for valuing options - Hook also uses it for its price suggestions - and we will plug in the following inputs for our case study:

- 08/09/2022 (mint date):

Average price (S): 0.42 ETH (OpenSea)

Note: Steve bought his DGDGKs for about 0.30 ETH, below average trading price on that day

Annualized volatility (σ) = 1297.76% - 09/01/2022 (press date):

Average price (S): 12.46 ETH (OpenSea)

Note: Steve sold his DGDGK #266 for 16 ETH

Annualized volatility (σ) = 619.68% - Interest rate (r): 2.87%

- Dividend yield (q): 0.00%

- Expiry: 30 days

- Strike: 40% above average price

Gas price calculation is omitted for this exercise.

Result

If instead of buying DGDGK #1306, 698, 460, 1657, and 266 on 08/09 and selling them over the next 24 hours and on 08/29 for a handsome 18.54 ETH profit (1272% of the 1.46 ETH invested capital), Steve instead purchased 30 day, 40% out of money call options because he thinks there is a good chance DGDGK might go to the moon, his returns could look like this:

Due to the fact that Steve’s hypothetical 30 day options are still 7 days away from expiration (09/08 vs. 09/01) and being deep in the money (12.46 ETH >> 0.59 ETH), the value of his options - which can be freely traded in the market - is equal to their intrinsic value (current average minus strike) plus time value (7 days from expiration).

If Steve were to sell his in the money call options for their option value or fair market value (FMV), it would result in a 59.35 ETH profit (2956% of the 1.94 ETH invested capital, vs. 2.10 ETH to buy at average price).

Again, it is important to keep a few of our assumptions in mind: It is possible that he would have to sell the options at a slight discount from their FMV depending on the market conditions, and it is also possible that he could underpay for the options on 08/09 since we took an aggressive volatility estimate (i.e., actual day-of volatility could be well below the 1297.76% estimate, making the options cheaper to purchase). But neither would meaningfully change the outcome we have computed above.

Summary

Call options offer traders who are bullish on a collection healthy exposure to the upside while requiring much less invested capital compared to buying the NFTs outright at market/average price.

If a portfolio NFT trader wanted to bet on a few high quality collections just in case one of them turns out to be the next DigiDaigaku, call options are well worth a serious consideration.

Learn more about how Hook is bringing call options to NFTs. Join Hook Discord or follow us on Twitter for future updates!